RBA

The Board of Reserve Bank of Australia (RBA) met on Tuesday 6th July 2021 to decide the monetary policy. The policymakers decided to provide ongoing support for the Australian economy. The goal is to achieve a low unemployment rate and keep the inflation rate consistent with the target range of 2 to 3 percent.

Despite the strong recovery in employment, the inflation and the wage growth outcomes remain subdued. RBA currently expects a temporary increase in inflation and wage growth. Inflation is expected to be 1.5 percent over 2021 and 2 percent by mid-2023. CPI inflation is expected to rise temporarily to about 3.5 percent over the year to the June quarter as the easing of COVID-19 related restrictions.

The RBA confirms that under its quantitative easing program, RBA will purchase $4 billion worth of government debt until at least mid-November. The current $100 billion round of purchase is due to end in September.

In particular, the decision includes:

- Retain the April 2024 bond as the bond for the yield target and retain the target of 10 basis points.

- Continue purchasing government and semi-government bonds after the completion of the current bond purchase program in early September. We will purchase $4 billion of bonds a week until at least mid-November.

- Maintain the cash rate target at 10 basis points and the interest rate on Exchange Settlement balances of zero percent.

Yield Target:

The 3-year yield target introduced in March last year during the pandemic aimed to lower the funding costs and support the economy. Now the maturity date for a 3-year bond has moved to April 2024. The Board decided to maintain the April 2024 bond as the target bond, rather than using the bond with a maturity date of November 2024. The Board also decided to remain the target of 10 basis points, which is the same rate as the target cash rate.

Bond Purchase

RBA will continue to purchase bonds given Australia has not yet achieved its employment and inflation objectives. However, the Board is responding to the stronger-than-expected economic recovery and improves outlook by adjusting the weekly amount purchased. Further review will be conducted in November and the Board will respond to the state of the economy at that time.

In late June, the final drawdowns under the Term Funding Facility were made. $188 billion has been drawn down under this facility in total, adding liquidity to the Australian banking system. The facility is providing low-cost fixed-rate funding of 3 years tenor and will continue to support low borrowing costs until mid-2024.

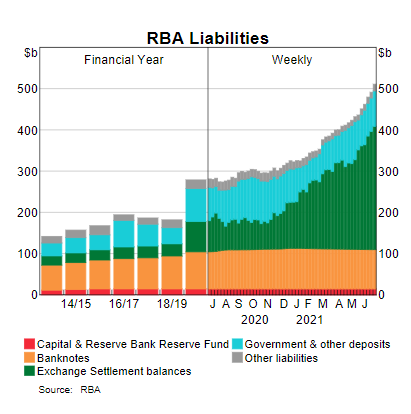

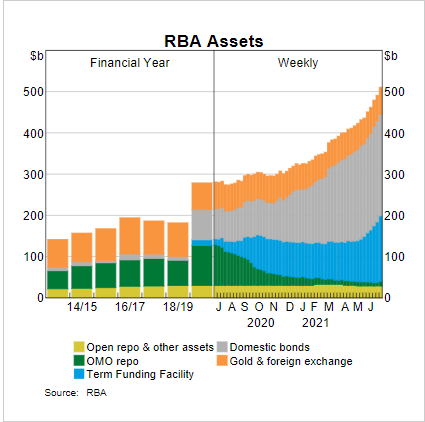

RBA Balance sheet (latest update on 7 July 2021):

Note: A repo is an agreement between two parties under which one party sells a security to the other, with a commitment to buy back the security at a later date.

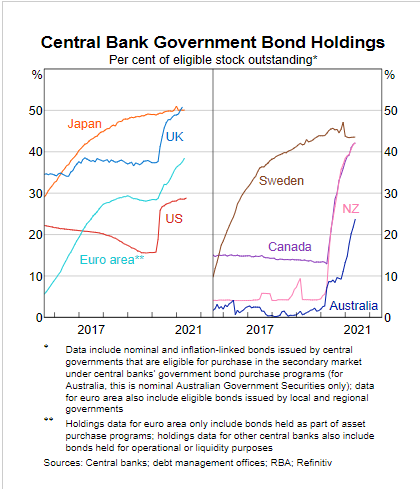

RBA government bond purchase (latest update on 7 July 2021)

Unconventional Monetary Policy

Unconventional monetary policy occurs when tools other than changing a policy interest rate are used. These tools include:

- forward guidance

- asset purchases

- term funding facilities

- adjustments to market operations

- negative interest rates

Asset Purchases

Asset purchases involve the purchase of assets by the RBA from the private sector and RBA pays for these assets by creating ‘central bank reserves’ (Exchange Settlement or ES balances).

RBA will set a target for the quantity of assets it will purchase or a target price of an asset. Quantitative Easing refers to the quantity target for asset purchase. RBA usually purchase assets in order to lower interest rate on risk-free assets.

The price target focused on the yield on a three-year Australian Government bond. RBA aims to achieve the target for three-year yield, which is the same as the cash target rate at 10 basis points.

The Quantity Target refers to the RBA purchasing a large amount of government bond, typically around 5 to 10 years maturity, issued by the Australian government and the state and territory government. The goal is to lower the interest rate at the right side of the yield curve (long term).

Term Funding Facilities

Term funding facilities involves RBA providing funding to financial institutions that are lower than the cost of most existing funding sources. It reduces the interest rate for borrowers and supports the supply of credit to the economy.

Cash Rate Target:

The cash rate is the interest rate on unsecured loans among banks. It is approximately equal to the risk-free benchmark (RFR) for AUD. Monetary policy decision involves setting a cash rate target and it is released at 2:30 pm after each RBA meeting.

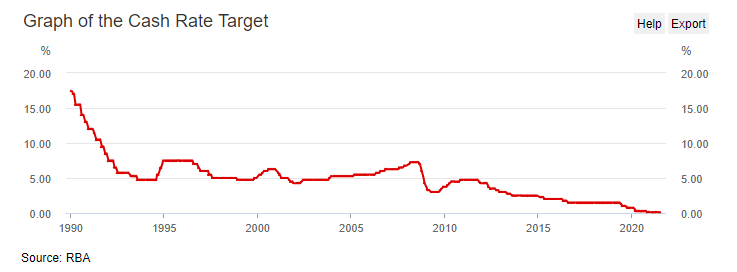

RBA’s past target cash rate:

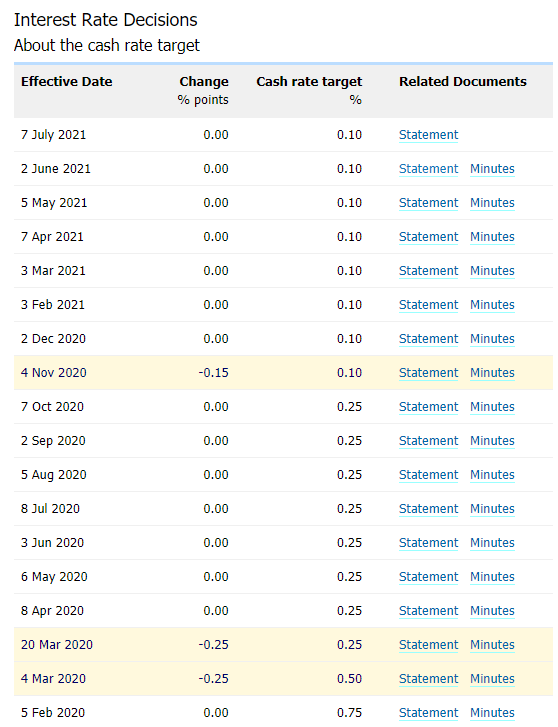

Recent Interest rate Decision:

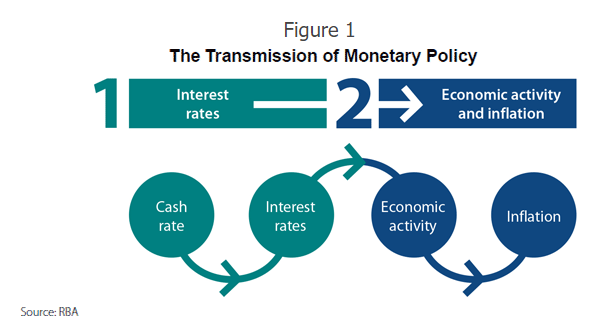

The Transmission of Monetary policy:

The RBA has an inflation target in a range between 2 and 3 percent on average. The cash rate is used to influence inflation in order to achieve this flexible medium-term target. The transmission of the monetary policy refers to how a change in cash rate impacts the interest rate in the market, economic activity, employment, and inflation.

When RBA lowers the cash rate (tightening monetary policy), other interest rates in the economy will fall. Spending is stimulated and business will increase lending and borrowing, resulting in an increase in economic activity. This will eventually lead to a higher inflation. A hike of interest rate a tightening of monetary policy) will have the opposite effect.

The transmission of monetary policy has two stages:

- Changes to the cash rate affects other interest rate in the economy;

- Changes in these economic activity and inflation affected by interest rates.

The transmission of monetary policy is also influenced by the market expectation of inflation. The higher expectations for inflation can lead to higher actual inflation.

Figures: The two stages of the transmission of monetary policy:

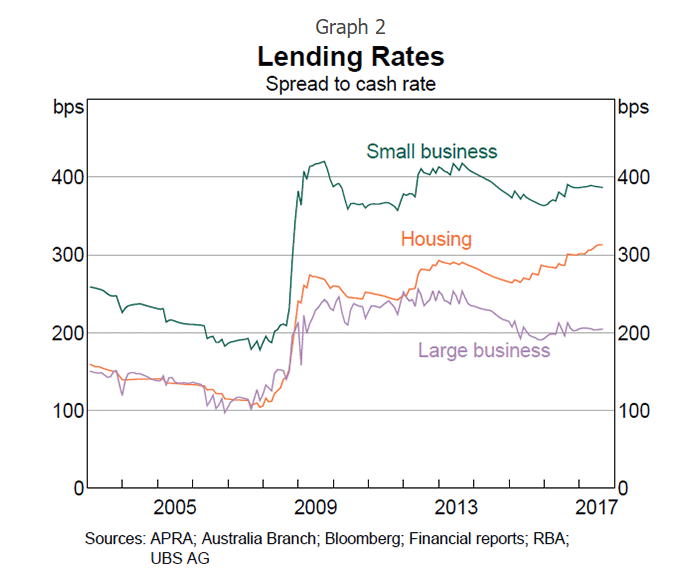

- The First Stage of Monetary Policy Transmission

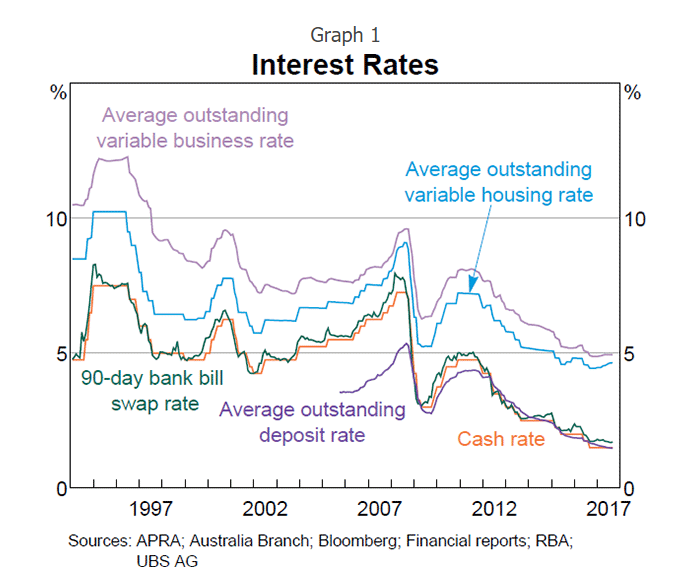

The first stage of monetary policy transmission refers to how changes to the cash rate affect other interest rates in the market. The cash rate is defined as the rate of interest which the RBA charges on overnight loans among commercial banks. The cash rate influences the funding cost of financial institutions, lending, and deposit rate for households and businesses.

The following graphs show the change in the interest rate and lending rate over time:

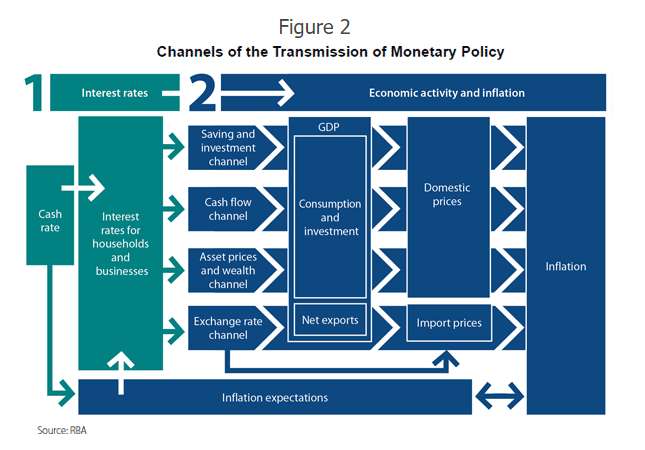

- The Second Stage of Monetary Policy Transmission

The second stage of transmission refers to how changes on interest rate influences economic activities, employment, and inflation. This occurs through various channels (Figure 2).

How will a reduction in interest rate affect different channels?

The cash flow channel

- For borrowers: lower lending rate will reduce the variable rate repayment they owe, resulting in a higher disposal income.

- For lenders: lower rates on interest-earning assets such as bonds and bank deposits will reduce interest income, resulting in a reduction in disposable income.

- In Australia, the cash flow channel is stronger for borrowers since the Australian household sector is a net debtor. Thus, a lower interest rate will lead to a higher cash flow in the whole Australian economy.

The asset price and wealth channel

- The wealth channel: a lower interest rate leads to higher demand of assets such as equities and properties, raising the prices of these assets. An increase in asset price will also increase the wealth of households and businesses, leading to more spending.

- The balance sheet channel: lower interest rate will increase the borrowing capacity of households and businesses.

The exchange rate channel

- A reduction in the cash rate will lower the interest rate in the Australian market relative to the rest of the world. The Australian asset will have a lower return relative to foreign assets, resulting in a lower demand of AUD and hence leads to a depreciation in the AUD.

- A depreciation in the AUD will reduce the price of Australian goods and services in the international market, resulting in a higher demand for Australian goods and services. In the meantime, foreign products services will be more expensive relative to domestic products. Thus, a depreciation in AUD will lead to a higher export volume and a lower import volume (higher net export)

- Depreciation in AUD will lead to higher imported inflation due to an increase in import prices.

Market Expectation

RBA reiterated that it will maintain the cash rate at its current all-time low until the labour market returns to the full employment, approximately low 4%, and inflation are in the target range of 2 to 3 percent, which is expected to be achieved by 2024. The next RBA meeting will be held on the 3rd of August.

Researchers suggest that RBA may be preparing for an adjustment on its cash rate earlier than the current guideline if the economic recovery continues to be strong. They also indicate that recent data flow suggests tighter policy next year is certainly possible.

Interest rate forecast from NAB:

References:

Cash Rate Target, RBA, https://www.rba.gov.au/statistics/cash-rate/

Today’s monetary policy decision, RBA https://www.rba.gov.au/speeches/2021/sp-gov-2021-07-06.html

The Transmission of Monetary Policy: How Does It Work? https://www.rba.gov.au/publications/bulletin/2017/sep/1.html

Unconventional monetary policy, https://www.rba.gov.au/education/resources/explainers/unconventional-monetary-policy.html

Central bank balance sheet and bond purchases, https://www.rba.gov.au/chart-pack/central-bank-balance-sheets-bond-purchases.html

RBA flags change to housing market and interest rates as economy bounces back, https://www.theage.com.au/politics/federal/rba-keeps-rates-unchanged-but-starts-winding-back-emergency-levels-of-support-20210706-p587b0.html