Welcome to our daily market update where we help keep you informed on the latest happenings in the world of FX and show you what this means for the Mighty Aussie Dollar.

If you have any questions or would like anything further explained, please don’t hesitate to reach out to your account manager or email info@cafx.com

Key Data Being Released Today

New Zealand – Business Manufacturing PMI (53.6)

New Zealand – Food Prices (-0.1% MoM)

South Korea – Current accounts

Macro Report

US CPI was release overnight and once again had beaten (already high) expectations with a 7.9% YoY vs 7.5% expected which was a 40 year high. Even with this high print it hasn’t taken into consideration the high prices of Oil yet.

Furthermore, the ECB announced overnight the asset purchase program would likely end in the Q3 which was faster than the market had anticipated and also the war in Ukraine would result in lower growth forecasts for the year, which shouldn’t come as a surprise.

All in all, the equity markets have turned red once again from the previous ‘dip buyer’ activity. Commodities has again seen further retracement after having sky rocketed the past few trading sessions.

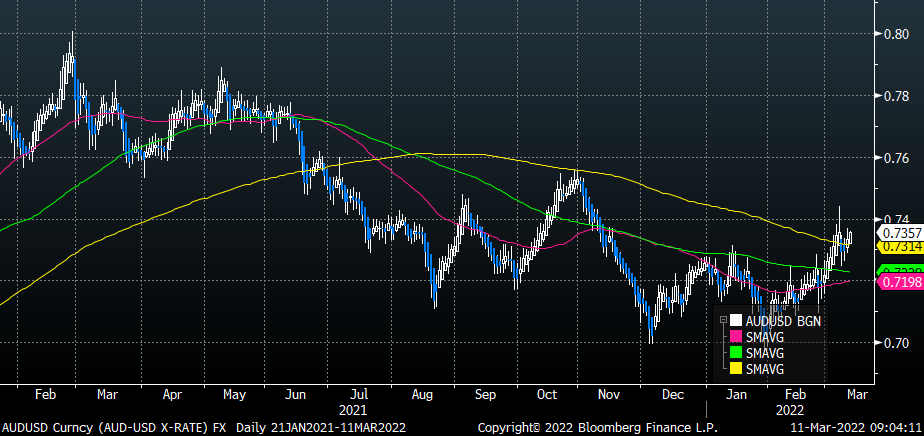

EURUSD has dropped overnight following market news as the USD slowly grinded higher against most of it’s G-10 peers. AUDUSD remains the standout though, even as commodity prices have seen a correction and USD bid, the high rates and risk on sentiment has seen the pair continue to edge higher with each trading session.

AUD/USD Daily Chart

DXY (USD INDEX) Daily

Major Global Markets

| Currencies | Level | Change (%) |

| AUD/USD | 0.7354 | -0.05 |

| AUD/JPY | 85.404 | -0.06 |

| AUD/CNH | 4.6524 | -0.07 |

| DXY | 98.5330 | 0.57 |

| Rates | Yield (%) | Change (%) |

| US 10 Year | 1.992 | 0.04 |

| Aus 10 year | 2.408 | 0.04 |

| Equities | Level | Change (%) |

| S&P 500 | 4260 | -0.43 |

| NASDAQ | 13591 | -1.10 |

| ASX 200 | 7131 | 1.10 |

| Commodities | Level | Change (%) |

| Iron Ore | 145.23 | -1.45 |

| Gold | 1996.9 | 0.22 |

| Brent Crude oil | 109.21 | -1.80 |